How Can I SECURE My Retirement?

Written by:

Tim Kenney, CFP®

Zoe Certified Advisor

In order to avert a government shutdown in December 2019, the government signed a spending bill that included legislation centered around retirement planning. The SECURE act, as it’s called, is the biggest revamp to the retirement system since the Pension Protection Act (2006). In 2020, the variety of changes will likely have varied consequences for soon-to-be retirees and those currently in retirement. Aside from the SECURE act, let’s take a look at some other retirement fund updates for this year:

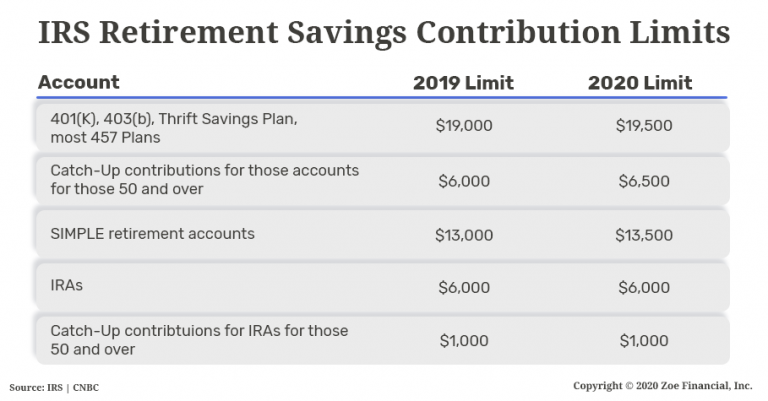

Some retirement contribution limits are going up in 2020 – don’t forget to increase your 401(k) and 403(b) deferrals and catch-up contributions for those over 50.

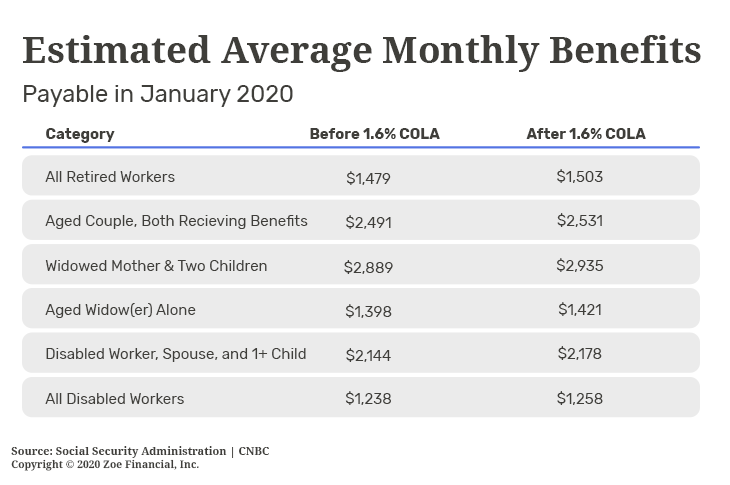

Social Security cost of living adjustments will increase payouts by 1.6% for 2020.

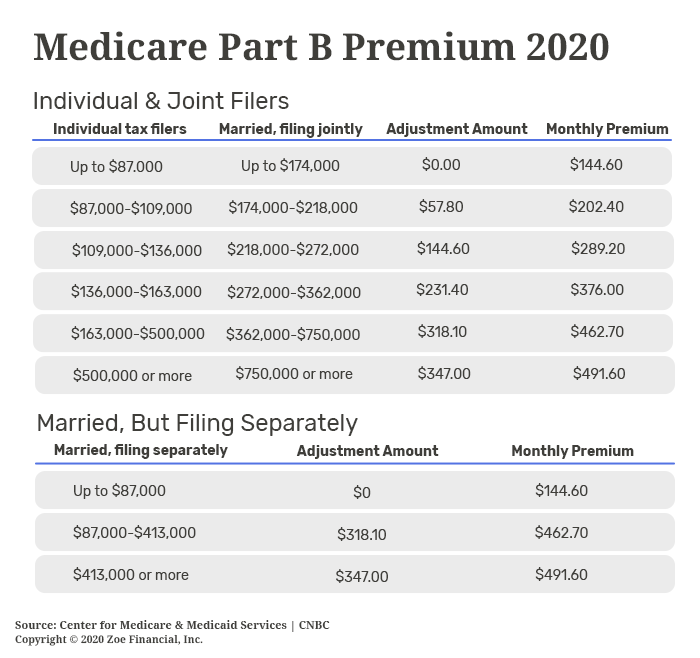

Finally, Medicare premiums went up somewhat significantly, especially for higher-income earners.

SECURE Act

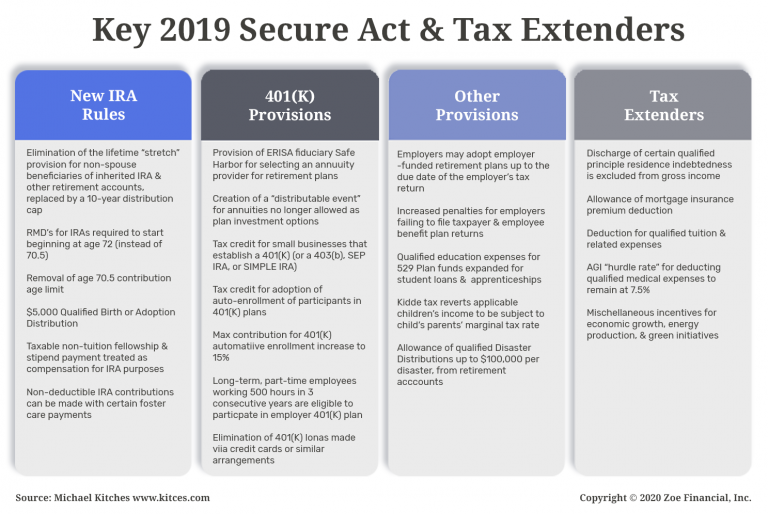

Now let’s get to the SECURE act, or Setting Every Community Up for Retirement Enhancement. The goal of the bill was to enhance retirement security around the country. There were quite a few provisions included in this legislation but these are the most impactful:

IRAs

Required Minimum Distributions Increased from 70 1/2 to 72

Increasing the age you must take distribution from your retirement accounts from 70 1/2 to 72 is a positive change. This will allow retirees who don’t need income from their retirement accounts to delay their taxable withdrawals and allow their accounts to grow tax-deferred for another 1 1/2 years. Plus, no more confusion on when you reach a 1/2 of age.

No More Age Restriction on IRA Contributions

Prior to this change, the law prohibited workers with earned income from contributing to their IRA’s past age 70 1/2. The SECURE act removes these restrictions allowing older workers to continue to contribute to their IRAs for as long as they have earned income (income derived from some kind of employment, not interest or trust income). With Americans living longer, there is an increasing number of people working much later than in the past. This is a positive change. Note – if you’re working past age 70 1/2 you’ll still need to take your RMD after age 72 regardless of if you continue to contribute or not.

Elimination of the Stretch IRA / 10-year Distribution of Inherited IRAs

A big one here – all non-spouse beneficiaries that inherit an IRA will be required to distribute all the assets in that account within 10 years. Prior to this, distributions were calculated by age and theoretically inherited accounts could be “stretched” to multiple generations depending on the dollar amount and age of the beneficiary. This allowed some ability to spread out the distributions and tax liability over the lifetime of the beneficiary.

The new law now requires those accounts to be completely distributed within 10 years. Those in their 40s and 50s inheriting retirement accounts from their parents might find themselves being forced to take big taxable distributions right in the middle of their peak earning years. Worse, if you’d done some estate planning and created a trust to be the beneficiary of their IRA with the intention of retaining control over timing and distribution, the new law renders your efforts moot.

*If you have worked with your attorney to name your trust as the beneficiary of your IRA you will need to review this.

Please note that this provision only pertains to non-spouse beneficiaries. Spouses, minors, and disabled/chronically ill individuals are exempt from the 10-year distribution rule.

You will probably start to hear more about the benefit of Roth conversions. Why? Roth IRAs do not have a required distribution age requirement for the owner. The Roth IRA can be left to a spouse, then left to their children which can let it accumulate for another 10 years before being required to distribute it under the new law. That distribution would be tax-free. This can get fairly complex due to the timing of taxes, Social Security, Medicare calculations, etc. For clarity, be sure to reach out to your financial advisor or CPA.

401(k)s

Annuities Now Allowed in Retirement Plans

I get it – the biggest risk for most retirees is outliving their money. Annuities are meant to protect people against that very risk. Who doesn’t want guaranteed income in retirement? Well, the insurance lobby was very involved in getting this legislation passed. Certain annuities offered by some of these insurance companies can be complicated, expensive, and potentially detrimental to the retirement plans of some people. Even worse – trustees of the 401(k) will not have the same fiduciary duty to offer annuities as they do in offering other mutual fund and ETF solutions.

Easing Some 401(k) Employer Requirements to Make Retirement Plans More Available

There are a handful of useful provisions in the bill designed to make 401(k)’s easier for employers to offer and workers to access. While most small businesses would love to offer retirement plans to their employees, prior laws made it difficult due to complexity, cost, and liability. Under the new law, small businesses will be able to pool together to offer multiple employer plans to help lessen their costs and fiduciary liability.

There will also be some opportunity for part-time workers to participate in 401(k) plans. The bill lowers the requirement to participate in a 401(k) plan to one full year with 1000 hours worked or three consecutive years with at least 500 hours.

Lastly – for small business owners, there are some pretty good tax credits offered to you to start a 401(k) plan. There is a tax credit to offset startup costs of at least $500 offered to you to start a 401(k) plan and in certain cases can add up to $15,000 over a few years! In addition, if you offer automatic enrollment to your employees you can receive an additional $500 over three years for $1500 total.

All in all, there are some pretty significant changes in this plan, both good and bad. However, being in the know can help your retirement significantly!

Still Have Questions?

Chat with the author of this blog, Zoe Network Advisor Tim K., CFP®