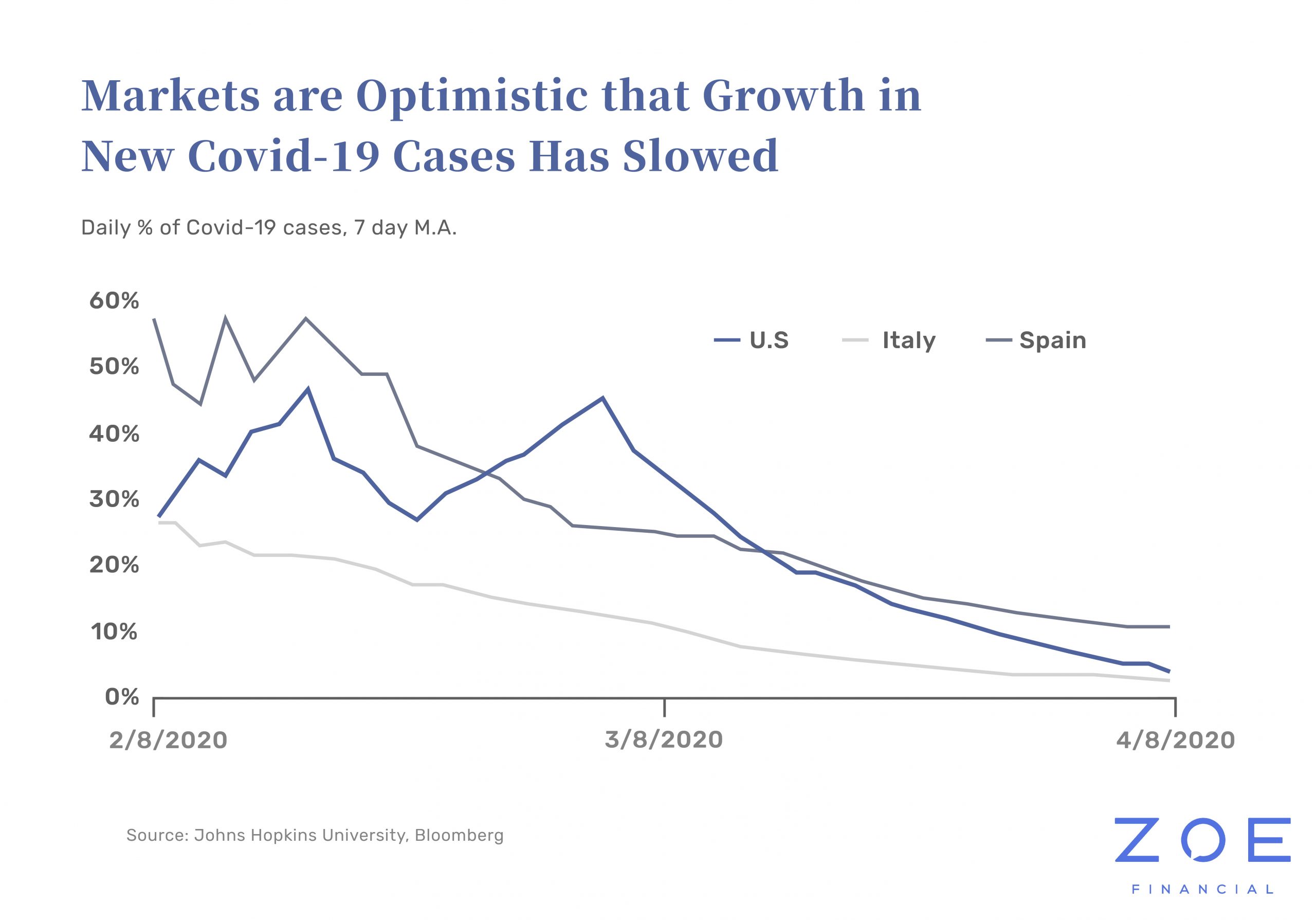

The news might seem a little incongruent recently, as stock markets recover while the number of coronavirus cases increases each day. Simply put, the market is currently aiming to price both how severe the shock is currently AND how strong the recovery will be. Stocks care about what will happen next rather than what’s already happened.

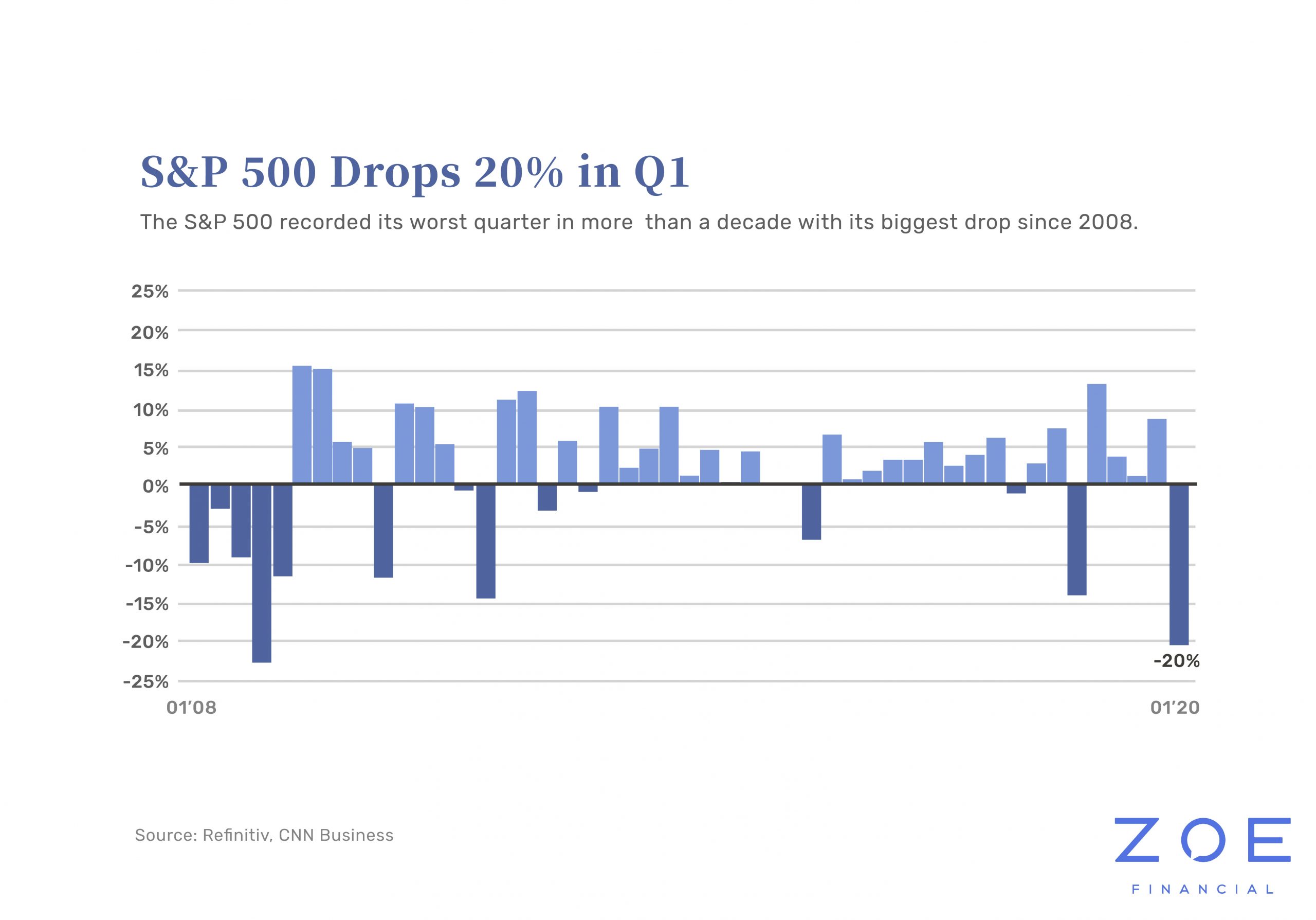

What Happened to U.S. Stocks?

Let’s start from the top: U.S. Stocks had the worst quarter (Q1 2020) in well over a decade. Stocks fell -20% from January to the end of March, and at one point they fell -34% from the highs to the low. In other words, by the end of March, the stock market was pricing in a really bad case scenario for April.